.jpg)

Private Equity Insights

Darien Group exists to bridge the gap between exceptional design capabilities and private equity communications. Our library of resources serves as a practical guide for firms looking to refine or redevelop their brand and ensure their story resonates with target audiences.

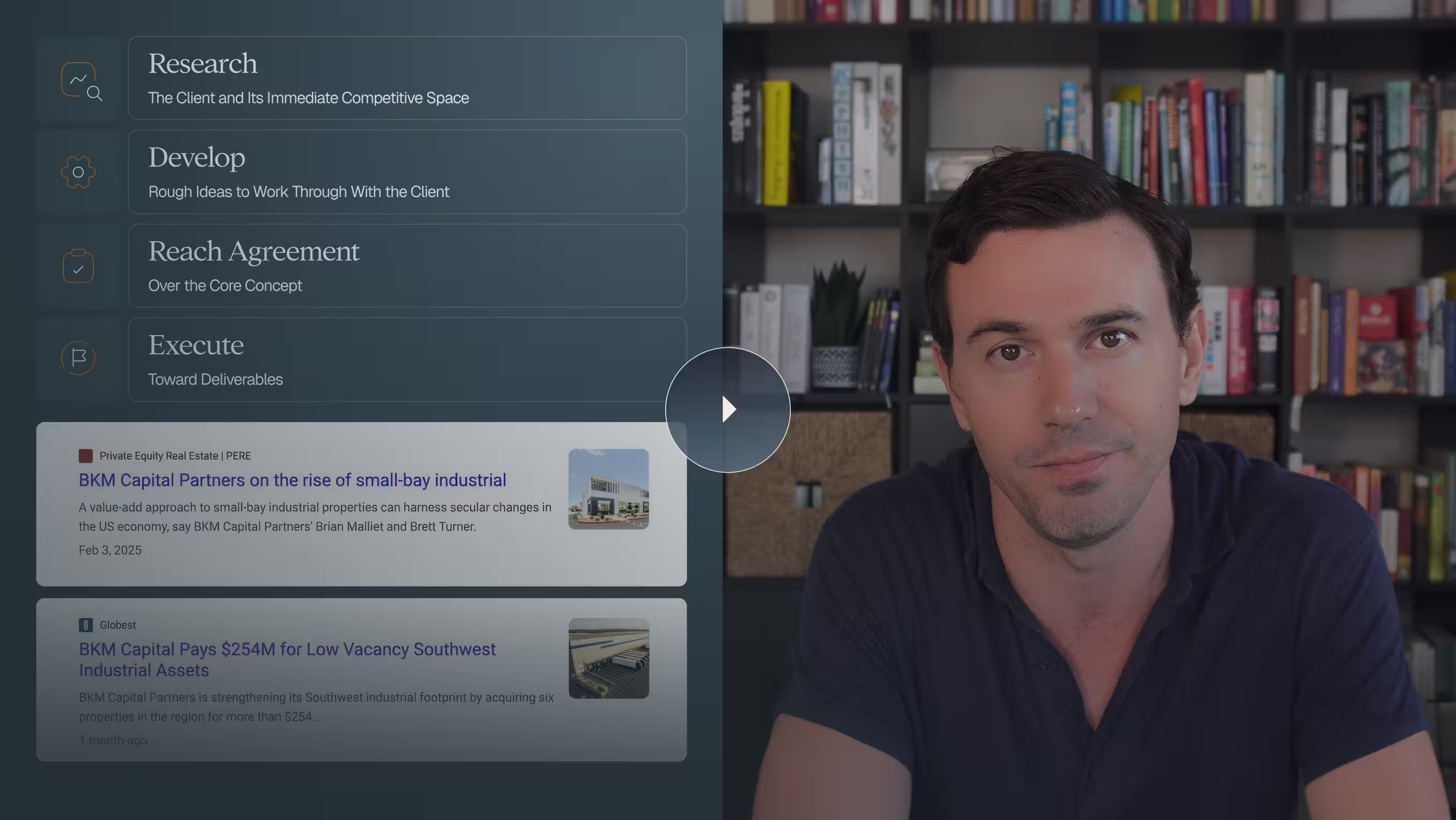

Featured Videos

Why clarity, design discipline, and site architecture now determine whether a product earns advisor mindshare

Over the past decade, real estate capital formation has steadily diversified into the wealth channel. RIAs, independent broker-dealers, wirehouses, advisor platforms, and high-net-worth individuals are now playing a growing role in non-traded REITs, interval funds, DST programs, and private vehicles structured for individual investors.

This shift comes with significant brand implications. Wealth-channel participants interact with information differently from institutional LPs, and they engage with materials in different formats and at different depths depending on context. As a result, managers expanding into this ecosystem often benefit from rethinking how their digital presence, collateral, and product communication are structured.

In the institutional world, the investment team “owns” the narrative. LPs read deeply, conduct heavy diligence, and often already have internal frameworks for evaluating real estate risk. In the wealth channel, the advisor owns the narrative, and often must communicate it to clients who may never read the deck, never attend a webinar, and never browse the website beyond a single page.

The burden on brand and communication is completely different.

Design matters more.

Clarity matters more.

Structure matters more.

And the bar for misinterpretation is significantly higher.

Why the Wealth Channel Behaves Differently

The wealth channel is not a monolith, but several consistent patterns influence how managers are evaluated and what a brand must accomplish:

- Advisors often act as intermediaries rather than end users.

They are evaluating not only whether they understand the strategy, but whether they can communicate it clearly to clients. Materials that require heavy translation create friction. - Many advisors are cautious about product selection.

Protecting client relationships is central to their role. When a manager is less familiar or a product is newer, clarity and design quality can help reduce perceived complexity. - Advisors manage significant information flow.

Time constraints mean many will review a factsheet or summary first before deciding whether to explore further. This heightens the importance of efficient, well-structured materials. - Products often compete in “menu environments.”

When advisors review a product, they commonly compare it to others available on their platform. These comparisons may happen quickly, so visual and narrative clarity play an outsized role in first impressions.

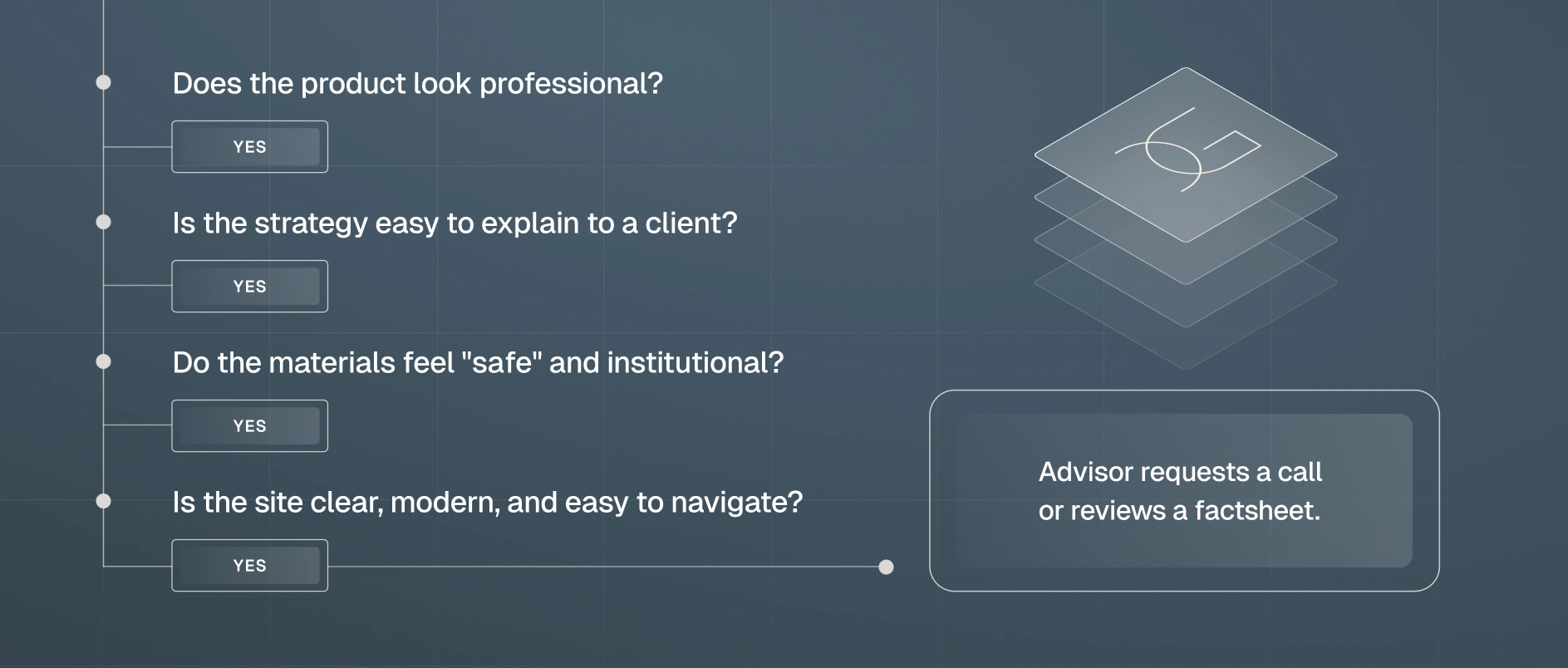

The Advisor Evaluation Process (Realistic, Not Idealistic)

If any step breaks, the product gets deprioritized.

The Brand Implications of Wealth-Channel Capital

The shift toward advisors changes not just the marketing layer, but the brand architecture that supports the product.

As Director of Brand Strategy at DG, these are the most important implications I see across our real estate clients:

1. Design Discipline Is Not Optional. It’s a Trust Signal

Clean design is evidence of operational maturity. Cluttered design or dated formatting has an outsized negative effect.

This is especially important in real estate categories where the underlying assets do not always photograph well — older multifamily, non-glamorous industrial, retail, or niche strategies. As discussed across DG’s RE series, poor photography can unintentionally shift perception more than teams realize.

For wealth-channel products:

- Typography must be readable.

- Layouts must feel institutional, not promotional.

- Disclosures must be visually integrated, not overwhelming.

- Exhibits must be simple enough to be screenshotted and passed along.

In this channel, design is the message. It communicates professionalism more quickly than the investment story itself.

2. Website Architecture Now Matters as Much as the Deck

Websites are often the first point of entry or impression of your firm among audiences in the wealth channel. They might:

- Google the product.

- Land on your website.

- Scan for 10–15 seconds.

- Attempt to understand the structure.

- Decide whether it feels institutional, clear, and credible.

This creates three requirements:

A. A dedicated microsite for each product (not buried inside the main firm website)

The parent website can remain institutional and thesis-forward.

The product microsite must be:

- simple,

- compliant,

- disclosure-heavy but digestible,

- visually clean,

- and easy for advisors to send as a link.

B. Navigational clarity

Avoid confusing menus, non-descript headers, and inconsistent user experiences.

The website experience should clearly guide the user to exactly where you want them to go and what they need to find.

C. A clear “Advisor Path”

Many advisors scan sites looking for:

- fact sheets

- share class details

- distribution history

- performance summary

- subscription mechanics

If they can’t find it quickly, they assume the manager isn’t ready for the channel.

The Four-Page Microsite Model

- Overview Page

- Introduce the product and its strategy in concise bullet points

- Why now, and why you

- Who it's for

- Clear product summary card

- Platform Page

- If the product is a part of a larger platform or parent company, clearly explain that relationship and leverage it as a differentiator.

- Portfolio Page

- Simple visuals

- High-level methodology

- Key exhibits

- Risk summary

- Shareholder/Advisor Resources

- Factsheets

- Subscription instructions

- Webinar replays

- Contact information

Anything beyond this should be optional, not required.

3. Messaging Must Be Cycled Down Without Being Watered Down

Advisors do not need a deep dive on:

- absorption patterns

- debt service dynamics

- submarket migration

- underwriting philosophy

- property-specific turnaround mechanics

They need a clean, high-resolution explanation of what the investment does and why it fits into a client’s portfolio.

Real estate managers often mistake “simplified” for “less sophisticated.”

In this channel:

Simplicity is a sophistication signal.

The messaging arc should cover:

- what problem the product solves

- how it behaves in a portfolio

- when it performs well

- how risk is mitigated

- how income is generated

- what the structure allows or prohibits

This is the clarity-first approach DG reinforces across the real estate series.

4. Wealth-Channel Products Require Their Own Visual Language

Institutional brands should feel strategic, investor-first, and thesis-led.

Wealth-channel brands require a different emotional calibration:

- calmer

- more conservative

- more spacious

- more “financial-professional” than “real-estate-operator”

- and with greater visibility around disclosures

This doesn’t require a new brand, but it does require a parallel brand system specifically engineered for the advisor environment.

This is one of the biggest mistakes managers make: they try to force institutional identity into a retail context.

The result is either too much gloss (seen as promotional) or too much complexity (seen as risky).

A separate visual system solves this.

5. Reporting Cadence Becomes Part of the Brand

Institutions are comfortable with quarterly cycles and asynchronous communication.

Advisors expect:

- monthly updates,

- clear thought leadership,

- clean NAV summaries,

- distribution clarity,

- quick-to-read news,

- and consistent templates.

Inconsistent reporting reads as disorganization, and in a channel where advisors are protecting client relationships, inconsistency is a non-starter.

How Advisors Internally Categorize Managers

“Clean and reliable”

→ Feels institutional

→ Easy to explain

→ Low perceived risk

“Good strategy, messy materials”

→ Harder to recommend

→ Increased advisor liability

→ Lower allocation likelihood

“Complex story, unclear materials”

→ Not worth the effort

→ Advisor defaults to bigger brands

The story matters, but the system that carries the story matters more.

6. Advisors Don’t Benchmark You Against Peers. They Benchmark You Against Platforms

Advisors compare materials to:

- Blackstone

- Starwood

- Carlyle

- Nuveen

- JLL

- Platform-approved giants

This means even smaller managers must look platform-ready, even if their product is newer or more specialized. Your brand and materials must do more heavy lifting.

Closing Thought

The increasing importance of the wealth channel is a structural shift in real estate capital formation. Managers who design their materials around the needs of advisors, not just institutions, tend to see stronger engagement. In this environment, brand is not merely aesthetic; it supports distribution by reducing friction and enhancing clarity. As more real estate strategies converge in messaging, managers who combine thoughtful design with well-structured communication will stand out long before a meeting is scheduled.

Why narrative clarity creates the most upside where few managers are looking

Real estate tends to move through recognizable cycles of allocator interest. When a sector is performing well, many managers focus their storytelling around it. When a category faces headwinds, such as hospitality or office in recent years, managers often communicate less actively while waiting for sentiment to stabilize.

At Darien Group, we believe overlooked and contrarian sectors often offer some of the clearest opportunities for managers who present a structured, measured point of view grounded in fundamentals and cycle awareness.

These strategies themselves aren’t new. What is evolving is how allocators evaluate them and the degree to which clear, well-sequenced communication can influence how a strategy is initially perceived.

Contrarian doesn't necessarily mean complex.

Overlooked doesn't necessarily mean underperforming.

And niche doesn't automatically mean “too small to be institutional.”

In many cases, these categories simply suffer from inconsistent framing or materials that create ambiguity rather than clarity.

Why Contrarian Sectors Struggle With Positioning

Contrarian strategies are rarely dismissed because the mechanics are flawed. More often, the narrative arrives without enough structure or context for an allocator to evaluate it efficiently. That perception forms early, often before the diligence formally begins.

Across overlooked sectors such as manufactured housing, RV parks, senior housing, certain retail categories, last-mile industrial, adaptive reuse, and cold storage, three challenges appear frequently:

- They sound “niche” even when the scale is institutional.

For instance, a manufactured-housing strategy may reach meaningful AUM, but if the narrative leans too heavily on terminology that evokes consumer stereotypes rather than investment characteristics, it can shape initial impressions in unhelpful ways. - Managers may overestimate how much pattern recognition LPs have in newer or less trafficked categories.

Many allocators have deep familiarity with multifamily or core industrial. Fewer have equivalent working knowledge of RV parks or cold storage. This simply increases the need for context and clarity. - Materials often drift toward extremes: too operational or too conceptual.

Operator-driven teams may emphasize micro-level details; finance-driven teams may rely too heavily on abstract language or dense data. The most effective narrative typically lives between the two.

The Early Moment That Shapes Perception

As noted in one of our previous posts, What Real Estate LPs Look For in the First 30 Seconds, LPs make their first judgments quickly, based on clarity, category fit, and institutional cues.

Overlooked sectors have a slightly higher burden at this early stage because the allocator is often trying to determine:

- Is this strategy appropriately sized and structured?

- Are the demand drivers intuitive based on the information provided?

- Does the manager present as investor-first vs. operator-first?

- How does the strategy relate to current cycle conditions?

When the materials lack structure or visual discipline, allocators may view the strategy as higher-risk than intended. Clear framing helps prevent that gap.

How LPs Sort Contrarian Strategies (A Simple Decision Map)

The key takeaway?

In contrarian categories, clarity determines whether the LP even considers the idea, not the strategy itself.

Where DG Sees the Biggest Opportunities

Below are four sectors where managers can unlock disproportionate benefits simply by structuring and presenting the strategy well.

1. Manufactured Housing

“Affordable housing with structural tailwinds” is not a thesis by itself.

Most manufactured-housing stories lean on affordability and supply-demand imbalance. A valid investment thesis, but not a sufficient or differentiated fundraising narrative.

What LPs actually want to know:

- What’s the consolidation opportunity?

- How fragmented is the market in your geography?

- Where does capex show up in NOI?

- How stable is tenancy compared to workforce multifamily?

- What are the regulatory dynamics?

A more compelling positioning ties these mechanics to investor outcomes:

Positioning Example (Stronger)

“We target supply-constrained regions where the delta between manufactured housing rents and Class B multifamily rents is widening, creating tenancy stability and predictable cash flow.”

Clear. Cycle-responsive. Repeatable.

2. RV Parks & Outdoor Hospitality

A category with powerful demographic drivers, but terrible storytelling.

This sector often suffers from one of two narrative extremes:

- overly lifestyle-driven (“people love the outdoors”), or

- overly operational (“we upgrade utility pedestals and optimize transient mix”).

Neither builds institutional trust.

What works:

- A demand-side argument (demographics, mobility trends)

- A supply-side argument (zoning constraints, limited new stock)

- Operational levers that drive NOI predictability (recurring revenues, membership programs)

- A clear explanation of seasonality and how it’s managed

A strong RV-park strategy often looks less like hospitality and more like annuity-like outdoor real estate, if the narrative is structured correctly.

3. Last-Mile Industrial Conversions

High-opportunity, high-friction — until articulated clearly.

Many managers describe these strategies as “creative repositioning,” which LPs interpret as entitlement or construction risk. The fix is simple:

Lead with the demand driver, not the physical conversion.

Example:

- E-commerce penetration in a specific metro

- Vacancy dynamics within 3–5 miles of population centers

- The pricing spread between obsolete flex and modern small-bay industrial

- The operator advantage in lease-up velocity

The strategy becomes far more investable the moment it’s framed as a logistics access story, not a building transformation story.

4. Cold Storage & Food Logistics

A sector defined by operational nuance, which is often buried or overcomplicated.

Cold storage is not a bet on temperature-controlled space. It’s a bet on:

- throughput efficiency

- tenant stickiness

- proximity to distribution nodes

- barriers to replacement

- energy efficiency and capex discipline

The challenge is expressing this without 40 pages of technical detail.

Here, sequence matters:

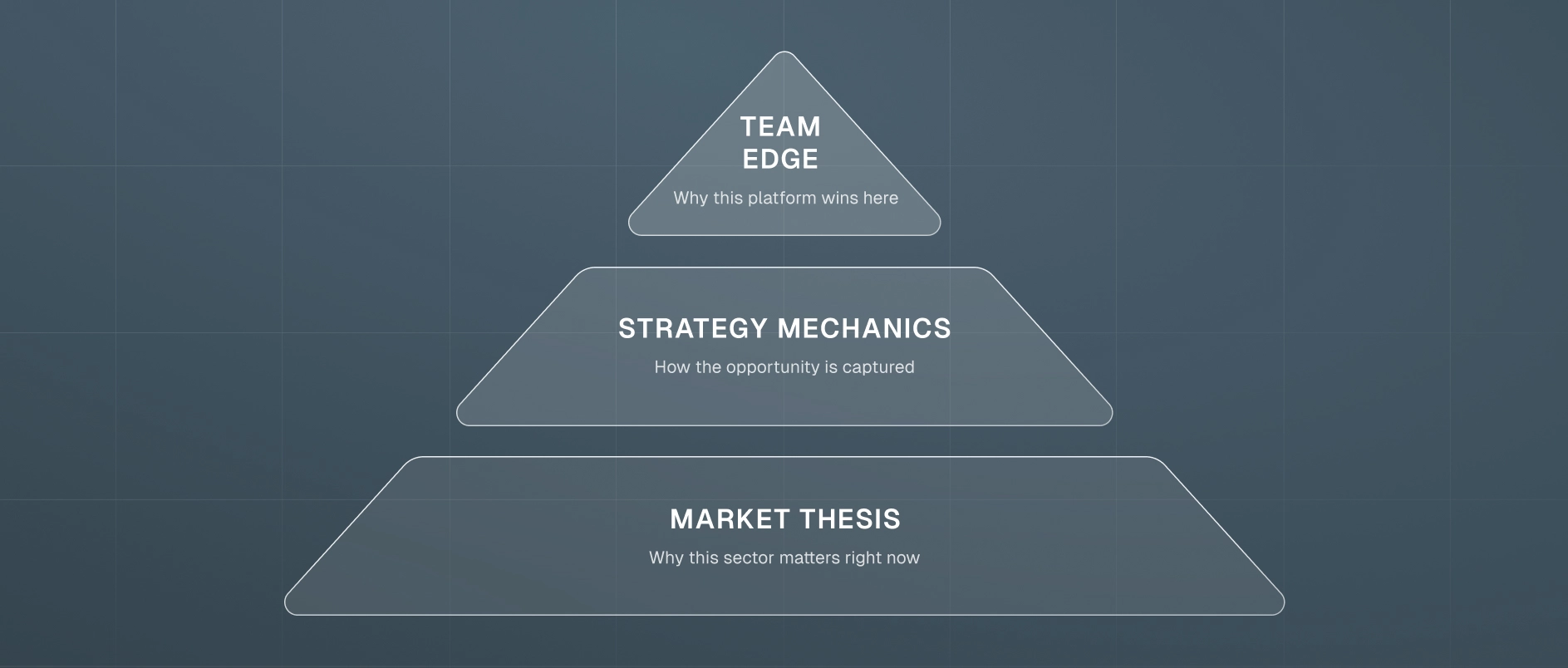

Cycle → Demand Drivers → Operational Differentiators → Geography → Team Edge

When the story is structured this way, the strategy feels less like infrastructure and more like a durable real estate allocation.

The Narrative Pyramid for Contrarian Sectors

Overlooked sectors fail when teams invert this pyramid, diving into operational nuance first, market dynamics last, and team fit not at all.

Why Contrarian Strategies Benefit Most From Professional Branding

Contrarian strategies often have more upside but also more perception risk.

That makes brand, materials, and clarity disproportionately important.

Here are three advantages we see our clients gain through stronger, more compelling storytelling:

1. A structured, cycle-aware thesis that feels rational, not promotional

Contrarian stories collapse when they sound defensive. They succeed when they sound analytical, structured, and grounded.

2. A brand system that avoids developer cues

Overlooked sectors are often operationally heavy. That creates risk of “operator” or “project” optics. A strong brand system neutralizes this immediately.

3. Materials that help LPs visualize the strategy, even in niche categories

Contrarian strategies require careful visual curation:

- fewer literal property shots

- more abstraction, process clarity, geographic logic

- better use of exhibits instead of paragraphs

Visual discipline makes unfamiliar categories feel investable.

Are LPs Able to Answer These Four Questions About Your Strategy Quickly?

- Why this sector now?

- What risk is priced? What risk is mitigated?

- Why is this team the right operator?

- How does this strategy behave across cycles?

If the materials don’t make these answers obvious within ~3 pages or one homepage view, LPs disengage, even if the underlying strategy is excellent.

The Opportunity: Narrative White Space

The biggest advantage for contrarian or overlooked strategies is simple:

very few managers tell these stories well.

Most rely on intuition or operator instinct. Very few build an institutional-grade narrative system that:

- clarifies the demand driver

- articulates the opportunity cleanly

- addresses the cycle responsibly

- positions the team as uniquely suited

- presents the information with discipline

That’s where the upside is.

Closing Thought

Contrarian and overlooked real estate sectors aren’t inherently niche; they are often simply less familiar. When the materials are modern, the framing is clear, and the investment case is presented with balance rather than defensiveness, these strategies can transition from peripheral to highly compelling. In real estate, clarity supports legitimacy, and in underexplored sectors, that legitimacy can translate into meaningful opportunity.

If you’ve ever been in a room with an institutional LP reviewing a pitchbook, you’ve probably noticed something that feels unsettling at first: they rarely read the slides the way managers imagine. They skim. They hop around. They glance at headlines. They flip back and forth. They study a chart or two and then jump ahead. And within minutes — sometimes even seconds — they begin forming an impression of whether the manager is worth deeper diligence.

This isn’t carelessness. It’s efficiency. Institutional LPs process a staggering volume of materials each year, often reviewing multiple decks a day during fundraising season. Their job is to determine — quickly — whether a manager has a real story, a real angle, and the organizational discipline to execute on it. The speed comes from necessity, not disinterest.

This is why skimmability is not a design preference or a stylistic choice. It is central to how LPs evaluate real estate managers. The best pitchbooks are engineered for this reality. The worst ones pretend it doesn’t exist.

LPs Don’t Read Pitchbooks Linearly

Most managers imagine an LP starting at slide one and making their way through the deck in a clean, sequential fashion. That may be true for a minority of readers, but more often LPs navigate the pitchbook the way someone navigates a newspaper or a magazine — they jump to whatever seems most relevant first.

One LP might skim the executive summary and move immediately to the portfolio examples. Another might check the strategy section and then flip to the team. A third might scan the first three slides, skip ahead to the track record, and then bounce back to the market thesis. This “pinballing” is not random. Each LP is trying to assemble the manager’s narrative as fast as possible: what they do, why the strategy makes sense now, and what the underlying risk profile feels like.

When a deck is built only for linear reading — slide one, slide two, slide three — it quickly loses these readers. A pitchbook must make sense even when read out of order, which means every major section needs its own internal logic. LPs should understand your point even if they encounter the slide in isolation.

Headlines Do More Work Than Most Managers Realize

Because LPs skim, the headline is often the only full sentence they read on any slide. A headline that simply labels the slide (“Market Overview” or “Value Creation”) forces the LP to interpret the underlying meaning themselves. Most won’t bother. They’ll form a loose impression and move on.

A clear, thesis-driven headline changes that dynamic. It tells the reader what the slide is actually trying to say. It shapes their interpretation before they get into the details. It gives them a frame for understanding the content that follows — even if they don’t read the content closely. And when you multiply that effect across 25 or 30 slides, the entire deck begins to feel more coherent, even if the LP never reads more than a small fraction of the text.

In categories like real estate — where so many managers sound alike — this is one of the simplest and most effective ways to differentiate. Most decks allow the LP to skim without absorbing anything. A good headline ensures the LP absorbs the right things.

LPs Look for Coherence, Not Comprehensiveness

Managers often assume that more detail equals more credibility. But LPs aren’t evaluating you on the volume of content — they’re evaluating how quickly they can grasp your strategy, your angle, and your level of discipline.

What LPs respond to is coherence: a market section that makes sense; a strategy that clearly responds to the environment described; a team that fits the needs of the strategy; exhibits that reinforce the points rather than distract from them; and an overall narrative that "clicks" early. When these elements align, LPs intuitively feel that the manager understands their own story.

When these elements don’t align — if the market section is generic, the strategy is unclear, the differentiators are buried, or the team appears before the reader understands why the team matters — LPs disengage quietly. They rarely say it out loud, but they sense the friction. And friction kills momentum.

Skimmability Isn’t Laziness — It’s Cognitive Reality

The way LPs read pitchbooks mirrors how all of us now read almost everything. No one sits down with a deck the way they sit down with a novel. They skim, scan, and jump to the sections that seem most relevant. LPs are simply doing it under higher stakes and tighter time pressure.

A skimmable pitchbook is not a shallow pitchbook. It is a disciplined pitchbook. It respects the reader's attention and increases the likelihood that the core message survives first contact. Managers who assume LPs will read every word are building for a world that no longer exists. Managers who build for skimming are building for reality.

Slides With Too Much Text Don’t Just Fail — They Create Distrust

Dense slides trigger an immediate negative reaction. LPs don’t read them, and more importantly, they start to wonder why the manager needed that many words. In real estate especially, verbosity often reads as a lack of clarity. It suggests the manager is unsure how to isolate their own thesis, or that they’re trying to cover every possible angle rather than making a confident argument.

LPs form quick impressions from dense slides. They may not articulate these impressions, but they’re powerful: the manager might be unfocused, overly academic, hiding behind jargon, or — even worse — spinning complexity that doesn’t need to be complex.

The irony is that the most complex strategies often require the cleanest slides. The more involved the process or the more unusual the asset class, the more efficiently the manager must communicate what actually matters.

LPs Notice What You Leave Out as Much as What You Include

Managers often fixate on what to add to the deck, but LPs are paying equal attention to what’s missing. If a pitchbook lacks a macro view, an angle, a clear differentiator, performance context, or a sense of why the strategy works now, LPs assume those things aren’t strengths. They fill in the blanks themselves.

The omissions often speak louder than the content. A pitchbook that says everything except why the manager is distinct is effectively telling the LP: “We are not distinct.” A pitchbook that says everything except how cycle positioning affects the strategy is effectively saying: “We are not thinking about timing.”

Editing is a core part of positioning. LPs understand this instinctively.

A Strong Deck Changes the Tone of the Meeting

You’ve noted this from your own experience: you can tell within the first ten minutes whether an LP is engaged. A well-constructed deck shifts the meeting from polite curiosity to genuine exploration. The LP asks more precise questions. They test your thesis instead of your clarity. They ask about portfolio construction, underwriting discipline, or acquisition criteria — not about the basics of what you do.

A weak deck produces the opposite effect. The LP remains at the surface, trying to decipher the fundamentals rather than evaluating the strategy’s merit.

Meetings break open when the deck has already done some of the work.

Closing Thought: Skimmability Is a Form of Respect

Managers sometimes fear that building for skimmability means diluting the story. But it’s the opposite. Real clarity is rare. LPs reward it because it is respectful of their time and protective of their attention. In a category where most materials feel interchangeable, a pitchbook that reads cleanly — even when skimmed — feels like a breath of fresh air.

Skimmability doesn’t simplify the story. It sharpens it.

In every real estate fundraise, two core documents do most of the communication work: the pitchbook and the PPM. They sit next to each other in the diligence stack, but they serve entirely different purposes. When managers blur the lines between them — trying to make the pitchbook do the PPM’s job or vice versa — the result is almost always negative. Either the pitchbook becomes bloated and unreadable, or the PPM becomes strangely thin and incapable of supporting real diligence.

Institutional LPs don’t talk about these documents the way managers do. They’re not thinking about how many slides belong in each or which charts go where. They read both through the lens of process discipline. The pitchbook is the orientation tool: a clear guide to what the manager is doing and why. The PPM is the verification tool: the full legal and narrative record of the strategy, the risks, the governance, and the economics.

When the roles are respected, the fundraise feels coherent. When they’re not, LPs quietly question whether the manager understands how an institutional fund process works.

Below is a practical look at how the pitchbook and PPM should relate to each other — and why managers so often undermine themselves by confusing the two.

A Pitchbook Is a Story. A PPM Is an Archive.

This is the single most important distinction.

A pitchbook tells a story; a PPM documents everything that story requires.

A pitchbook is:

- short,

- skimmable,

- narrative-driven,

- focused on the decision frame,

- and designed for asynchronous reading.

A PPM is:

- long,

- comprehensive,

- legal in tone,

- compliance-heavy,

- and built to provide full, formal disclosure.

The pitchbook exists to create comprehension and interest. The PPM exists to protect both sides from misunderstanding and to satisfy the internal and external stakeholders involved in a capital commitment.

When managers try to load their pitchbook with pages from the PPM — twenty pages of macro, legal disclaimers repurposed as slide content, or highly detailed operational language — the pitchbook collapses under its own weight. Conversely, when managers attempt to use a thin PPM to “keep things simple,” LPs wonder what else might be missing.

These are not interchangeable documents. They are a narrative and its source material.

A Good Pitchbook Distills. A Good PPM Expands.

The instinct among newer managers — especially first-time fundraisers — is to treat both documents as comprehensive. They try to say everything everywhere. But institutional LPs don’t want comprehensive pitchbooks. They want coherent ones.

A strong pitchbook distills the fund’s essence into:

- the reason this asset class matters now,

- the reason this team is equipped to execute,

- the reason this strategy works in this environment,

- and the reason the LP should care.

It does not attempt to replicate all the data in the PPM. If something needs ten pages of exposition, it belongs in the PPM. If something can be communicated visually or summarized in a single slide, it belongs in the pitchbook.

One of the clearest mistakes in real estate fundraising is when managers take a consultant-written market section from the PPM (often 20–40 pages long), shrink it into tiny text, and drop it into the pitchbook. LPs don’t read it. It doesn’t persuade them. And it breaks the rhythm of the entire deck.

The pitchbook should read like a guided tour.

The PPM should read like a reference library.

LPs Don’t Confuse the Two — But They Judge Managers Who Do

LPs use pitchbooks and PPMs in different ways:

The pitchbook:

- shapes first impressions,

- structures the first meeting,

- orients the diligence process,

- and communicates the angle.

The PPM:

- supports internal memo-writing,

- provides legal grounding,

- governs compliance,

- and supplies depth where needed.

LPs know the difference instinctively. They are not confused about which document does what. But they absolutely judge managers who create ambiguous boundaries between the two.

A pitchbook cluttered with risk disclosures signals sloppiness.

A PPM missing risk disclosures signals something worse.

A pitchbook crammed with 15 pages of macro signals a lack of narrative control.

A PPM lacking macro context signals an underdeveloped thesis.

A manager who gets these wrong does not look “less institutional.” They look uncertain.

Why Too Much Detail Hurts the Pitchbook (But Helps the PPM)

Real estate managers tend to be operators at heart. They want LPs to understand the operational nuance: the property tours, the negotiation mechanics, the underwriting models, the property management efficiencies. These things do matter — but they don’t matter in the pitchbook.

Operational nuance belongs in:

- the PPM,

- the appendix,

- or the meeting itself.

When nuance overwhelms the pitchbook, LPs lose the thread. They skim, they disengage, or they mistakenly assume the strategy is more complicated than it needs to be. That’s not because complexity is inherently bad — it’s because complexity, when poorly sequenced, feels like obfuscation.

The PPM, on the other hand, is meant to absorb complexity. It is supposed to contain all the nuance, all the disclosures, all the detail that substantiate the claims in the pitchbook. It is the grounding document — dense but necessary.

The pitchbook persuades by clarity.

The PPM persuades by completeness.

Use the PPM to Protect the Manager’s Narrative Discipline

Counterintuitively, the PPM is the tool that allows the pitchbook to stay clean. When managers understand that every detail has a home — just not in the pitchbook — they feel freer to keep the deck focused. They can put the macro deep dive, the operational diagrams, and the technical nuance where they belong: in the PPM.

This is where the documents start to work together. The pitchbook sets the argument; the PPM backs it up. A well-written PPM prevents a pitchbook from ballooning into a 70-slide monster built out of fear that something might be “missing.”

One of the highest compliments LPs give — usually indirectly — is when they describe a pitchbook as “clean.” Clean does not mean simple. It means the manager had the discipline to put each piece of information in the right place.

The Pitchbook Should Be a Decision-Making Frame

The pitchbook is not the diligence. It’s the frame through which diligence flows.

A strong pitchbook answers five implicit questions:

- What is happening in the market?

- What is the strategy?

- Why this team?

- Why now?

- What will this look like in a portfolio context?

Everything else either lives in the appendix or the PPM.

When managers respect this boundary, the deck becomes a tool that LPs can use — not a burden LPs must sift through.

A pitchbook should create the motivation to read the PPM.

A PPM should validate the motivation created by the pitchbook.

Closing Thought: A Pitchbook Isn’t Short Because It’s Shallow. It’s Short Because It’s Sharp.

Real estate managers often assume that more detail equals more credibility. But institutional LPs don’t equate detail with conviction. They equate clarity with conviction. A pitchbook’s job is to make the story legible. A PPM’s job is to make the story defensible.

The separation between the two documents isn’t bureaucratic — it’s strategic.

It allows the manager to communicate the right amount of information to the right audience at the right moment in the process.

The managers who understand this distinction are the ones whose materials feel clean, confident, and genuinely institutional.

Spend enough time reviewing real estate pitchbooks and you start to see a consistent pattern: there are only two categories. Decks that look and feel institutional, and decks that don’t. And the divide has very little to do with design vocabulary or stylistic preference. It’s about the signals that design quality sends to an audience that reviews hundreds of these materials each year.

Institutional LPs don’t use the language of designers. They don’t talk about kerning or color theory. But they are exceptionally quick at making judgments about professionalism, discipline, and operational maturity. In a pitchbook, design is rarely the story — but it is always part of the psychology.

This creates a strange dynamic in real estate, a category where many managers come from operator or development backgrounds rather than allocator backgrounds. They may be excellent investors, but design is not a natural skill set. And when the pitchbook looks like a 10-year-old template or something assembled by whoever “knows PowerPoint,” LPs draw conclusions far beyond the aesthetic.

Below is a candid look at the design standards that actually matter to institutional LPs, why they matter, and how managers can present themselves with the level of polish investors instinctively expect.

Professional vs. Amateur: LPs Know the Difference Instantly

Most managers underestimate how quickly an LP can tell whether a deck was built professionally. They don’t need to identify the font or critique the color palette; they can simply feel whether the materials look and behave like institutional tools.

The most common red flag is not outdated taste — it’s dated templates. Slides that look like they came from a 2012 PowerPoint file. Generic gradients. Clipart-level icons. Mismatched shapes and colors. Charts pasted in from Excel without any reformatting. Image crops that are slightly off. A deck that looks “stitched together.”

These details may seem trivial, but they accumulate into a very clear impression:

If the manager didn’t invest in presenting their strategy cleanly, where else have they underinvested?

This reaction is not fair in every instance, but it is extremely common.

The good news is that professional design is not difficult or expensive to access. A manager doesn’t need a six-figure agency to create an institutional-grade pitchbook. They simply need someone — internal or external — who understands how to produce clean, modern slides. Someone who knows how to apply basic discipline. Someone who understands that design communicates far more than style.

Institutional Design Isn’t Ornate — It’s Clean

There is a misconception that institutional design means decorative design. In reality, institutional LPs respond to simplicity, not flair.

A premium, mature deck usually has the following characteristics:

- Clean slides with clear hierarchy.

Not walls of text, not ornamental shapes. - Charts that match the visual brand.

Not screenshots from other documents, not mismatched fonts. - Photography that is strong (or intentionally omitted).

Real estate is visual, but bad visuals hurt more than no visuals. - Consistency across slides.

Colors, spacing, image treatments, and layouts should feel coherent.

None of this requires a designer with an MFA. It requires good judgment and discipline. LPs are not looking for beauty — they are looking for maturity.

Photography: A Differentiator When Used Well, a Liability When It Isn’t

Real estate has an inherent advantage over private equity: the asset class is tangible. If the assets photograph well, photography is one of the fastest ways to build connection and credibility.

But this only works when the assets support the story. If the properties are tired, dated, or visually unappealing, showing them hurts more than it helps. Many managers underestimate this dynamic. They assume “showing the real thing” always wins. It doesn’t. LPs form impressions quickly, and mediocre imagery creates subconscious skepticism.

When the assets are strong, show them proudly. When they’re not, build a more abstract visual identity. This is one of the most important judgment calls in real estate materials — and one of the most overlooked.

Design Signals Something Deeper: Discipline

Pitchbooks do not need to be visually innovative. But they do need to be visually disciplined. Discipline is the underlying signal LPs are responding to. Clean decks imply clean thinking. Consistency suggests operational maturity. A professional visual system suggests a manager who is organized, structured, and attentive.

Messy design sends the opposite signal. LPs wonder:

- If the materials look disorganized, what does the underwriting process look like?

- If the visuals are sloppy, how tight is the property management discipline?

- If the pitchbook feels like a patchwork, what does this say about reporting?

None of these implications are necessarily accurate, but LPs make quick, subconscious leaps. In real estate especially — where operator competence is paramount — the leap is hard to avoid.

Avoid the “Broker Memo” Aesthetic at All Costs

Real estate operators often communicate using the same artifacts they use internally: deal memos, OM packets, broker marketing summaries, zoning diagrams, floor plans, maps with arrows. These materials serve a purpose inside the real estate ecosystem, but they are disastrous in fundraising.

Broker memos are dense, cluttered, and unfriendly to non-operators. They assume familiarity with local markets and deal mechanics. They make sense to someone who spends their days touring properties—not someone trying to evaluate an investment strategy across dozens of managers.

When a pitchbook resembles a broker packet, LPs silently categorize the manager as unsophisticated or underprepared. Even if the underlying strategy is compelling, the materials undermine it.

Pitchbooks must be decks, not OMs. They must feel investable, not transactional.

“Institutional Design” Does Not Require Design Vocabulary

Real estate managers sometimes worry they don’t have an eye for design, and they often don’t have a designer in-house. That’s fine. LPs are not grading aesthetic nuance—they’re grading whether the materials feel professional.

Institutional design is not:

- ornate,

- flashy,

- hyper-stylized, or

- filled with dramatic typography.

Institutional design is:

- clean,

- consistent,

- modern,

- unforced.

It is the absence of distraction.

It is the presence of coherence.

A pitchbook that feels effortless is usually the product of someone who knew what to remove, not what to add.

Use Design to Support Skimmability

LPs skim — sometimes aggressively. Good design helps them do this without missing the thread.

A skimmable pitchbook uses:

- clear, thesis-driven headlines,

- visual breathing room,

- layouts that reveal the point quickly,

- and slides that can be understood in a few seconds.

Bad design works against skimming. The eye doesn’t know where to go. Key points get buried. The hierarchy collapses. When LPs skim a messy deck, they lose the narrative — not because the story wasn’t good, but because the design didn’t help them find it.

Skimmability is not just about writing. It is about design that respects how people actually read.

Design Doesn’t Win the Mandate — But It Can Lose It

No LP commits to a fund because the pitchbook is beautiful. But LPs do walk away from managers whose materials feel amateurish or inconsistent. They don’t always say it directly, but you feel it in the lack of follow-up, the muted enthusiasm, or the subtle shift from curiosity to polite disengagement.

Design does not create conviction.

But it does create permission for conviction.

A good deck opens the door wide. A sloppy deck makes the LP second-guess whether they should step through it.

If you lined up 50 real estate pitchbooks from 50 different managers, you’d see something unsettlingly consistent: almost all of them sound the same. The phrases, the diagrams, the sequencing, even the vocabulary — much of it is interchangeable. “Vertically integrated.” “Hands-on value creation.” “Market knowledge.” “Proven team.” “Deep pipeline.” It’s no one’s fault. It’s just the gravitational pull of a category where many strategies look directionally similar.

But institutional LPs, family offices, and advisors aren’t evaluating managers as if they are equal. They are trying to understand who stands out in a category that often doesn’t differentiate itself. A pitchbook that reads like everyone else’s isn’t neutral — it’s negative. If everything sounds the same, the LP assumes (fairly or unfairly) that nothing is distinctive about the manager.

Differentiation in real estate is rarely about inventing a new vocabulary. It’s almost always about going one level deeper — past the surface-level language that everyone uses and into the underlying mechanics, culture, or track record that actually separates one firm from another.

Below is a practical look at how real estate managers can create pitchbooks that actually sound like them — not like a template the last ten managers used.

Start From the Assumption That You Sound Like Everyone Else

This may feel harsh, but it’s the most liberating starting point. Most real estate managers begin the pitchbook process from the wrong mental model: “Here’s what makes us different.” The problem is that many managers have very similar backgrounds, similar strategies, similar asset types, and similar processes. When the strategic DNA is similar, the language almost always converges unless you actively intervene.

So the better starting question is:

“What could we say that 50 other firms can’t?”

Sometimes the answer is clear — unusual experience, an uncommon geographic footprint, a distinct sourcing method, or a market thesis that isn’t mainstream. Sometimes it’s more subtle — cultural DNA, a founding story, or a pattern of performance that tells a story other firms can’t replicate. And sometimes it’s not obvious until you dig: a specific operational capability, a technique in underwriting, a data-driven wrinkle, or some aspect of the team’s history that is quietly powerful.

You don’t need dozens of differentiators. You need one or two that are real and defensible. The pitchbook’s job is to elevate those above the noise.

The Best Differentiators Translate Strategy Into Investor Outcomes

This is one of the clearest gaps you identified: real estate managers often talk about their strategies in inward-facing terms. They describe what they do instead of what those actions mean for the investor. Operators, in particular, fall into this trap because they’re so used to speaking to lenders, brokers, developers, or other operators who already understand the mechanics.

Institutional LPs are reading for something different. They want to understand how your specific approach delivers outcomes that differ from the market’s baseline. They’re not trying to become experts in your process; they’re trying to understand the effect of your process on risk, return, and portfolio construction.

So instead of:

- “We are vertically integrated,”

try: - “Because our property management is in-house, we compress the timeline between operational issues and corrective action.”

Instead of:

- “We use a hands-on approach,”

try: - “Our team’s background in X–Y–Z enables faster improvements in NOI during the first 18 months of ownership.”

Instead of:

- “We have strong local relationships,”

try: - “We see off-market deals earlier, which affects both pricing and competitive posture.”

These are small shifts — but they change the deck from a list of internal competencies to a list of investor-relevant outcomes.

Make the Executive Summary Do the Hard Work

Differentiation usually succeeds or fails in the first two pages of a pitchbook. This is where institutional LPs begin to decide what your three “memorable things” are. If you don’t choose those for them, they choose for themselves — and the default choices are rarely flattering.

A strong executive summary:

- isolates the one or two differentiators that matter most,

- presents them directly, not buried inside paragraphs,

- ties them to the market context,

- and gives the reader a reason to care before they slog through the details.

For later-vintage managers, the summary must convey credibility and continuity. For first-time or second-time managers, it must convey legitimacy. For managers in crowded categories, it must convey a difference. For managers in emerging niches, it must convey investability.

The supporting slides can carry nuance. The opening slide must carry memory.

Property Images Aren’t Decoration — They’re Differentiation Tools

Real estate has one built-in advantage over private equity: tangibility. LPs can see what you're investing in. They can imagine themselves standing in front of the assets. The more the asset class lends itself to visual connection — industrial, multifamily, hospitality, office conversions — the more important it is to use that to your advantage.

But the rule is simple: If the assets photograph well, use them. If they don’t, don’t.

Few things undermine a pitchbook faster than mediocre images of mediocre assets. If your assets don’t elevate the brand, the visuals should become more abstract and more brand-led.

When the imagery is strong, it creates instant connection. When it isn’t, it creates doubt.

Understand What Differentiation Actually Looks Like to LPs

Differentiation is not about unusual vocabulary. It’s about unusual clarity.

LPs skim. They flip. They search for the thread that feels most real. They have a decade of experience with managers claiming the same things. And they’re trying to determine whether your story has any internal friction, any mismatches, or any false notes.

Differentiation sounds like:

- a market thesis that isn’t recycled,

- a sourcing angle others can’t plausibly claim,

- performance patterns that actually match the stated strategy,

- geographic focus that feels intentional instead of generic,

- or a firm history that creates a coherent narrative arc.

You don’t need all of these. You need one or two. But they must be hard-edged and specific, not vague or interchangeable.

The job of the pitchbook is to help the LP find that specificity without digging.

Differentiate by Restraint, Not Excess

One of the fastest ways to undermine differentiation is by overwhelming the reader with detail. Real differentiation requires editing. The pitchbook should avoid three common traps:

- Process bloat. Too many diagrams, too many arrows, too many bullet points.

- Market-section overreach. Macro is important, but 20 slides of macro overwhelm the story.

- Overuse of jargon. Some LPs know the category deeply—but many don’t want to decode technical language while skimming.

Great pitchbooks feel intentional. They show the manager understands not only what makes the strategy work but how to communicate it without drowning the reader.

The Most Important Differentiator: A Coherent Angle

Every manager has a story. The problem is that most stories are told indirectly or inconsistently. A differentiated pitchbook has an angle — a point of view that shapes the entire narrative.

That angle might be:

- a market dislocation the manager understands better than peers,

- a sourcing method that consistently uncovers mispriced assets,

- a capability gap the team fills uniquely well,

- or a long history of execution in a niche others find too small or too complex.

Whatever the angle is, it must be explicit. LPs cannot intuit it from between the lines. The pitchbook must introduce it early, reinforce it through the structure, and land it again at the close.

When the story is clear, differentiation feels effortless. When the story is fuzzy, everything sounds generic.

Closing Thought: Differentiation Lives in the Details LPs Actually Remember

Institutional LPs see hundreds of pitchbooks. They are not impressed by ornate phrasing or unusual adjectives. They don’t need a brand-new vocabulary. They read for coherence, confidence, and specificity. They want to know what is genuinely yours and why it matters.

Differentiation in real estate is about finding the one or two things that no one else in the room can plausibly claim — and building the pitchbook around them. Not loudly, not theatrically, but with enough clarity that the LP walks away remembering exactly why the manager matters.

That is the real work of differentiation.